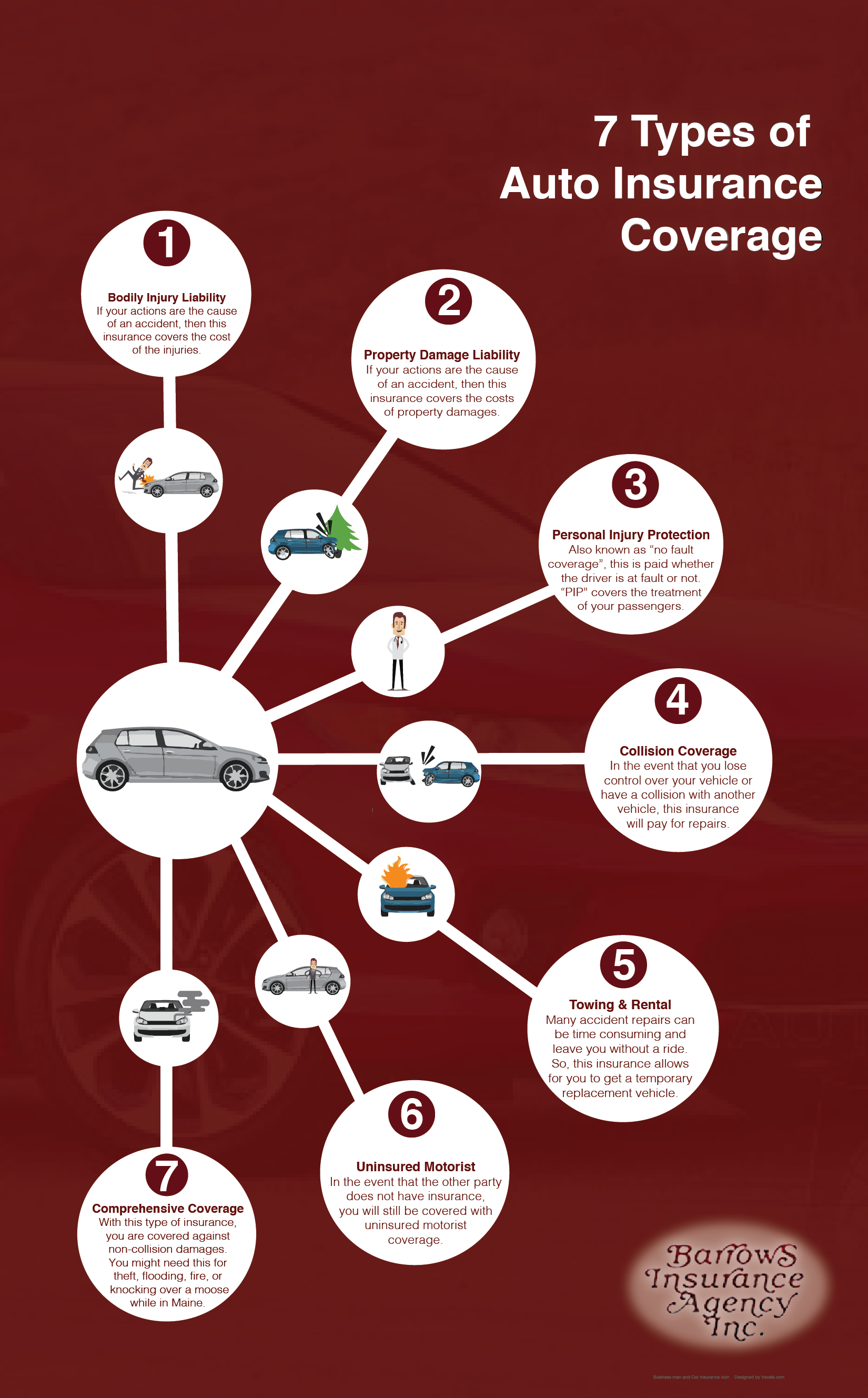

Massachusetts RV Insurance

Recreational vehicles can be a adventurous way to live your life…or spend your weekend away. Getting the right insurance, will ensure that your happy weekend isn’t ruined by lack of coverage. Massachusetts RV insurance isn’t difficult. With a little understanding, you will be able to have an informed conversation with your insurance agent.

Classes of RVs

Given the wide range of vehicles that classify as an RV, there are different classifications: Class A, B, and C. Depending on what type of RV you own and how often you are using it, your insurance options will vary.

To give you some idea of each class, let’s look at some examples:

- Class A: motor coaches, luxury coaches, and converted buses

- Class B: smaller RVs without cab-overs, travel-trailers, camper vans, and converted cargo vans style campers

- Class C: cab-over styled campers, separate cab area, and fifth wheel vehicles.

Typical Coverages for RVs

First of all, an RV is still at risk for the same things your car is, so the same coverages apply: collision, comprehensive, and liability. At the same time, the vehicle is a living space. Therefore, some of the same coverage as your homeowners insurance are needed, such as coverage on your personal belongings. In addition, other coverages will vary by agent and your specific needs, but may include:

- total-loss replacement

- emergency expense

- roadside assistance

- towing

- campsite

- vacation

- full-time usage (if you travel and live in your RV)

- uninsured/underinsured motorist

- permanent attachments

While that is a laundry list of coverages, your insurance agent will be able to walk you through the process of determining your specific needs and coverage levels.

How Much Does Massachusetts RV Insurance Cost?

Prices for Massachusetts RV insurance can vary widely, depending on two very RV-specific factors:

- Your RV Class – Classes A & C are the most costly, respectively. Finally, Class B is usually not as costly.

- Usage – If you live in your RV, the cost will naturally rise with the level of risk.

Additionally, your insurance costs will rise if you have a poor driving record, if you need additional coverages, or if you want certain limits and deductibles. Due to your personal needs, costs are very specific to you. A ballpark figure in RV insurance might be $500 – $2,500 per year, but any of the aforementioned aspects could raise or lower your RV insurance costs.

Next Steps

Insurance on your investment is a no-brainer, even when it is parked. Yet, when you have your RV on the road, Massachusetts requires that you have insurance with at least liability coverage. So if you have purchased or are purchasing an RV and would like to have a conversation with an agent, you can contact us here and one of our friendly staff members will be happy to help you.